June 2026 | flhomebuyers.com

Florida's housing market has flipped. Sellers who two years ago could name their price are now cutting $30,000, $50,000, sometimes six figures to get a contract signed. The forces behind this aren't temporary. They're structural, they're compounding, and for a growing number of homeowners, they've turned the cost of holding a property into something worse than the loss of selling one.

I work these deals across South Florida every week. The holding-cost math most sellers run too late is the part that changes minds.

Your Monthly "Holding Tax"

Before anything else: a framework.

Every month you hold a Florida home you plan to sell, money leaves your account and doesn't come back. Insurance, property taxes, maintenance, the interest portion of your mortgage, all of it piling up while values in most metros keep sliding. I call the combined figure your Holding Tax. It's the single most important number in your sell-or-hold decision.

Here's what it looks like for a real scenario: a Cape Coral single-family home bought in 2022 for $420,000 with 5% down.

| Monthly | |

|---|---|

| Mortgage interest (6.5% on ~$387K balance) | $2,096 |

| Insurance ($8,292/yr Florida avg) | $691 |

| Property taxes (Lee County w/ homestead) | $350 |

| Maintenance reserve | $200 |

| Value decline (-2.4% YoY on $345K current value) | $690 |

| Monthly Holding Tax | $4,027 |

Over 12 months, that's $48,324 gone.

Compare that to selling today at a 10% discount off current value: a $34,500 hit. Painful, but $13,824 less painful than holding another year while the property bleeds.

Breakeven sits at about 8.6 months. If you're confident the market recovers enough to erase $4,027/month within that window, hold. Cape Coral-Fort Myers values are still declining 2.4% year-over-year, and insurance premiums aren't dropping.

Make your own call, but make it with the real number in front of you.

Calculate yours:

| Your numbers | Monthly |

|---|---|

| Mortgage interest (check your amortization schedule or latest statement) | |

| Homeowners insurance (annual premium / 12) | |

| Property taxes (look up at your county property appraiser / 12) | |

| HOA / CDD fees | |

| Maintenance and repairs | |

| Monthly value change (estimate from Zillow or recent comps) | |

| Your Monthly Holding Tax |

Enter monthly costs as positive numbers. If your property is gaining value instead of falling, enter that value-change line as a negative number.

Keep this number. You'll need it.

If You Own a Condo Facing a Special Assessment

This is where the market pain concentrates hardest. After the Champlain Towers South collapse killed 98 people in Surfside on June 24, 2021, Florida passed SB 4-D (signed May 2022), banning condo associations from deferring structural maintenance. Buildings three stories or taller now need a Structural Integrity Reserve Study (SIRS), and associations can no longer waive reserves for structural components.

56% of Miami-Dade condo associations are non-compliant as of early 2026. Statewide, only 36% of 11,270+ applicable associations had self-reported compliance. To close the funding gap, buildings are billing owners directly.

Mediterranean Village in Aventura hit residents with $400,000 per unit. Cricket Club in North Miami: $134,000. 1060 Brickell levied $21 million building-wide, roughly $40,000-$50,000 per unit across two 45-story towers, triggering a board recall and court-ordered new leadership.

Monthly HOA dues in South Florida now run $600-$900+ in many buildings. Statewide, the median fee rose from ~$232 to ~$390 since 2022, a 68% increase in three years. Condo inventory sits at 8.6 months statewide and 13.2 months in Miami-Dade. Balanced is 4-5.

"Jingle mail" (mailing the keys back to the lender) is growing among retirees who can't sell and can't pay. Many buildings sit on Fannie Mae and Freddie Mac mortgage blacklists, which can shrink the buyer pool and put pressure on resale value. Starting August 3, 2026, Fannie Mae eliminates the Limited Review path for projects with 10+ units, and minimum reserve allocation rises from 10% to 15% in January 2027.

What you can do

1. Sell before the assessment records. If your building hasn't levied the assessment yet, you have a window. Once it's on the books, every buyer sees it and prices accordingly. Check your building's status through the DBPR online portal. Florida law requires sellers to disclose assessments they're aware of, including those discussed in board meetings within the prior 12 months. Selling beforehand won't make you whole, but it limits the damage.

2. Push for HB 913 alternatives. HB 913 (signed June 2025) lets associations vote for a 2-year pause on reserve contributions if the building completed a milestone inspection within the prior 2 years. But the vote requires a majority of TOTAL voting interests, not just those present at the meeting. A 200-unit building needs 101 votes regardless of attendance. HB 913 also lets buildings use loans or lines of credit instead of lump-sum assessments, and raised the mandatory reserve threshold from $10,000 to $25,000. If your board hasn't explored these options, push for a meeting. You have the right to attend all board meetings (48-hour advance notice required, posted on property).

One thing to understand: you cannot individually opt out of a validly approved special assessment. Nothing in Chapter 718 allows it. Once the vote passes, every owner pays their share based on the allocation method in the declaration.

3. Request a payment plan. Most boards will offer installment plans for special assessments. A $100,000 assessment at $2,000/month over 50 months is survivable. You don't need to accept the first schedule the board proposes. Negotiate terms, ask if the association is pursuing a loan (which spreads costs differently), and attend the budget meetings where these decisions get made.

4. If you're in Miami-Dade: apply for the county loan program. Miami-Dade relaunched its Condominium Special Assessment Loan Program in June 2026, offering low-to-zero-interest loans for building recertification and mandatory repair costs. Requirements: owner-occupied, homesteaded, primary residence, income at or below 140% of Area Median Income. Priority for seniors 62+. Call 786-469-4100 or email condospecialassessment@miamidade.gov. If you're in another county, check with your local housing and community development department for similar programs.

5. Explore financing before draining savings. FHA Title I Property Improvement loans cover up to $25,000 for single units. If you have equity, a home equity loan or HELOC can finance the assessment at 6-11% instead of taking the cash hit all at once. Seniors 62+ in FHA-approved buildings may qualify for a reverse mortgage (FHA HECM for Condos, max claim $1,249,125 in 2026). Check your building's approval status at the HUD condo lookup tool.

6. If you want to challenge the assessment: Assessment disputes are excluded from DBPR arbitration under F.S. 718.1255, so you'd go to circuit court. Grounds include procedural failures (inadequate notice, no quorum), improper allocation, or board breach of fiduciary duty. Do NOT withhold payment while disputing. Associations have expedited lien and foreclosure powers regardless of pending disputes. Get legal advice first. The Florida Bar Lawyer Referral Service offers 30-minute consultations for $25 max: call 1-800-342-8011. Low-income residents can use Florida Free Legal Answers.

7. Contact the Condo Ombudsman. The state Office of the Condominium Ombudsman handles complaints about financial records access, election disputes, and procedural SIRS questions. They can investigate statutory violations and the Division of Condominiums can fine associations up to $5,000 per violation. Call 954-202-3234 or email ombudsman@myfloridalicense.com.

8. Request and review the actual SIRS report. It's an official association record. Your building must provide a copy or notify you it's available for inspection within 45 days of receiving the study. If they refuse, submit a formal written request. They have 10 business days to comply. If they still won't, file a complaint with DBPR. You can hire an engineer at your own expense to review the report for aggressive assumptions or technical errors, then present findings to the board.

If Your Roof Is Killing Your Sale

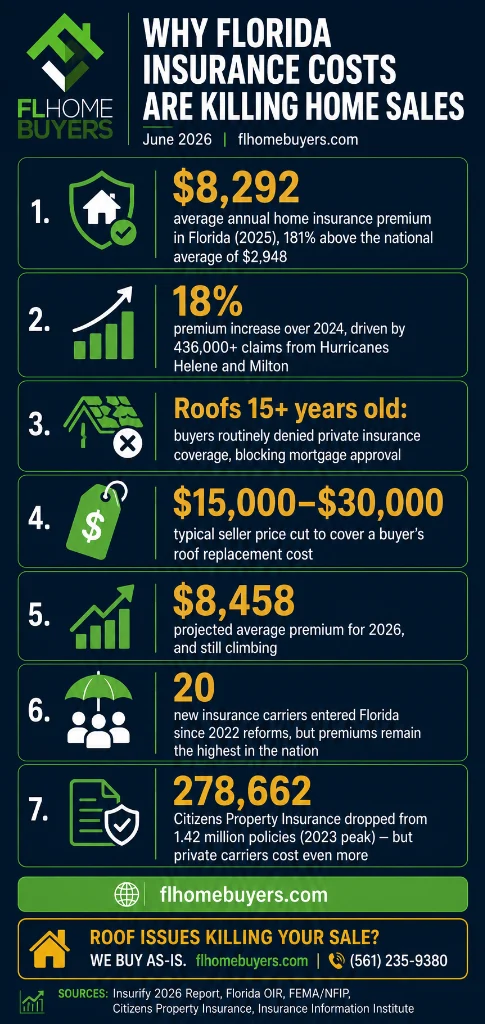

Florida is the most expensive state to insure a home. Average annual premium: $8,292 per Insurify's 2025 report, 181% above the national average. Hurricanes Helene and Milton pushed combined claims past 436,000, with NFIP flood claims generating close to $7.5 billion in payouts. Those losses feed straight into renewal pricing.

But the bigger problem for sellers isn't the premium itself. Insurance rules can derail financing before closing.

Under Florida Statute 627.7011, insurers can't refuse coverage based on roof age alone if it's under 15 years. In practice, many carriers flag roofs at 10 years for inspections. A roof over 15 that can't demonstrate five years of remaining useful life through a professional inspection can create underwriting problems. If the buyer cannot obtain acceptable insurance, mortgage approval and closing timing can be affected.

Sellers then face the choice of replacing the roof, negotiating a credit, reducing price, or finding a buyer who will take the roof issue as part of the written terms. The right number depends on roof material, age, permit history, local code requirements, insurance options, and contractor pricing.

Reform is helping on the carrier side. Citizens Property Insurance peaked at 1.42 million policies in October 2023 and has since shrunk to ~278,662, with an 8.7% rate cut taking effect July 1, 2026. Twenty new carriers entered after the 2022 reforms (SB 2-A killed one-way attorney fees and banned post-loss assignment of benefits), and reinsurance came in 15-25% cheaper at June renewals. But lower reinsurance costs haven't reached the seller with a 2004 shingle roof in Cape Coral. Premiums are still high compared with many states, and older roofs still trigger denials.

What you can do

1. Apply for My Safe Florida Home. My Safe Florida Home offers a free wind mitigation inspection and matching grants up to $10,000 for hardening improvements (roof-to-wall connections, secondary water barrier, impact windows, reinforced garage doors). The state puts in $2 for every $1 you spend, so your $5,000 can qualify for the full $10,000 grant on a $15,000 project. Low-income homeowners (at or below 80% of your county's Area Median Income) get up to $10,000 with no match required. The 2026-2027 cycle has $405 million in funding through the General Appropriations Act.

Three things most guides leave out:

It's a reimbursement program. You pay the contractor first, then submit documentation for the grant money. Budget for the upfront cost.

Do not sign a contract or start work before receiving a formal award letter. Starting early can disqualify a project or create reimbursement problems, so verify the current program rules before work begins.

The timeline can run for months from application to reimbursement, and the queue changes as funding opens and closes. Check the current My Safe Florida Home status before making a sale plan around the grant. If you need to sell quickly, the reimbursement timeline may not match your deadline; if you have more time, it may offset part of the roof or wind-mitigation cost.

Eligibility: single-family detached or qualifying townhouse (not condos), active homestead exemption, building permit issued before January 1, 2008, insured value $700,000 or less.

2. Get a wind mitigation inspection before listing. Costs $75-$150. It documents your roof's wind resistance features and can cut the windstorm portion of a buyer's premium by 10-45%. Here's where the savings come from:

| Feature | Estimated windstorm premium reduction |

|---|---|

| Opening protection (impact windows and shutters on every opening) | 30-45% (all-or-nothing: every opening must qualify for full credit) |

| Hip roof (sloped all 4 sides) | 28-32% |

| Secondary water barrier (SWR) | High value per dollar; added during re-roof for $500-$2,000 extra |

| Roof-to-wall connections (clips or wraps vs. toe nails) | Significant; varies by connection type |

Each carrier files its own discount structure with the OIR, so exact numbers vary. By law, your insurer must provide a "Notice of Premium Discounts for Hurricane Loss Mitigation" showing your specific credits. Ask your agent for this document.

Best strategy if you're replacing the roof anyway: get the SWR, upgraded roof deck attachment (enhanced nailing), and improved roof-to-wall connections all done at the same time. Marginal cost during a re-roof is low compared to the premium savings over 5-10 years.

Homes built 2002 or later often qualify for default credits without upgrades. Handing a buyer a mitigation report at the first showing removes the insurance question from the negotiation.

This is different from a four-point inspection, which covers roof condition, electrical, plumbing, and HVAC and is required by most carriers for homes 20-30+ years old. You want both. Bundle them with the same inspector ($75-$200 for a four-point, $75-$150 for wind mitigation). Common four-point red flags that fail a home: recalled electrical panels (Federal Pacific, Zinsco), polybutylene plumbing, active roof leaks, and non-functional HVAC.

3. Get a roof certification if you're approaching 15 years. A written certification from a licensed inspector showing 5+ years of remaining useful life prevents automatic denials and keeps your buyer pool open to financed purchasers.

4. Check Citizens and private-carrier rules before assuming the buyer pool is gone. Citizens Property Insurance and private carriers use roof-age, condition, inspection, replacement, and underwriting rules that can change. A roof certification, current insurance quote, or written replacement plan can matter when buyers are trying to finance a Florida house with an older roof.

5. Know the seller credit caps before you list. If you plan to credit the buyer for a roof instead of replacing it yourself:

| Loan type | Max seller credit |

|---|---|

| Conventional (5-10% down) | 3% of purchase price |

| Conventional (10-25% down) | 6% |

| Conventional (25%+ down) | 9% |

| FHA | 6% |

| VA | 4% |

On a $350,000 sale with an FHA buyer, that's a $21,000 cap. If the roof costs $25,000, you need a $4,000 price reduction on top of the credit.

6. Tell your agent about FHA 203(k) loans. Buyers using an FHA 203(k) can roll the roof replacement cost into their mortgage, borrowing against the home's after-repair value. Limited 203(k) covers up to ~$75,000 in non-structural rehab. The renovation funds go into escrow and release as the work is completed. This expands your buyer pool because the buyer doesn't need cash for the roof at closing. Not every lender offers 203(k), but the ones that do give your listing access to buyers who would otherwise walk away. Fannie Mae's HomeStyle Renovation loan works the same way for conventional borrowers.

7. Sell as-is to a cash buyer. Cash buyers do not need buyer-side insurance approval to close, and there is no appraisal contingency or lender-mandated repair list. The tradeoff is price: a cash offer usually discounts for repair cost, resale risk, and the buyer's margin. Compare the written cash net against the retail net after repairs, credits, commissions, insurance, utilities, taxes, and time.

If You Can't Compete with Builder Prices

Traditional sellers aren't competing with each other anymore. They're competing with D.R. Horton and Lennar, both of which have in-house mortgage companies and the budget to buy down rates.

62% of builders nationwide offered sales incentives in June 2026, the 15th consecutive month above 60%, and 35% cut base prices an average of 6%. D.R. Horton is sitting on 22,900 unsold homes and called out "increased market softness in pockets of Florida" on their earnings call. Lennar ran incentives at 12.9% of deliveries. Both offer 2-1 buydowns through captive lenders, so a buyer walks in at 3.99% year one.

46.2% of U.S. home sales in May 2026 included seller concessions, a record. Orlando ran hottest at 58.6%, up from 38.3% a year earlier.

Panama City Beach is down 5.8% year-over-year, Gainesville dropped 4.7%, Cape Coral-Fort Myers came in at -2.4%. Zillow's statewide number sits at $377,578, off 3.3% from last year.

What you can do

1. Price to the comps, not to what you paid. This is one of the most common mistakes I see in deals that stall. Sellers anchor to their 2022 purchase price and list above current comps. The property sits, takes price cuts, and often sells below where it could have moved if priced correctly on day one. Pull the most recent sold comps you can find, then adjust for condition, concessions, insurance friction, and builder competition.

2. Offer your own concessions. You can't match a builder's rate buydown dollar-for-dollar, but closing cost credits ($5,000-$15,000), a home warranty, or a repair allowance all work. Buyers respond better to concessions than to a straight price reduction, even when the math is identical, because concessions reduce their cash-to-close while a price drop just changes the number on paper. Structure them so they show in the MLS.

3. Target buyers who care about what builders cannot offer. Cash investors care about cap rate, rent comps, condition, and exit value. Some second-home buyers care more about established neighborhoods, mature lots, verified flood history, or location than builder incentives. The point is to market the property’s real advantage instead of trying to out-discount a builder.

4. Get a pre-listing appraisal. Costs $400-$600. Gives you a realistic number before you commit to a listing price and prevents the deal from collapsing at the buyer's appraisal. If you know the appraised value upfront, you price from transparency instead of hope.

One piece of context: pending sales are recovering. Single-family pendings were up 4.8% year-over-year in May 2026, and condo pendings rose 9.0%. Buyers are transacting. But they're transacting at their price, not the seller's.

If You're Underwater on Your Mortgage

Charlotte County (Punta Gorda) ranked #1 on ATTOM's Q1 2026 Housing Risk Report, scored on foreclosure rates and underwater mortgage concentration. Eleven other Florida counties landed in the top 50, more than any other state.

Florida's unemployment hit 4.8% in May 2026, above the 4.3% national average, with payroll gains flat. Pandemic-era migration dried up: net domestic migration dropped to 22,517 people for July 2024-June 2025, down from 310,000+ in 2022. Fewer people moving in means fewer buyers.

ATTOM counts 113,813 "seriously underwater" properties in Florida, where the loan balance tops market value by 25% or more. A year ago, 49.3% of Florida homes were equity-rich; that's down to 43.2%. Cape Coral-Fort Myers has given back about 18% from its 2022 high, and Orlando came in 5.6% below last year.

Florida had the worst foreclosure rate in the nation in May 2026: 1 in every 2,110 housing units got a filing, versus 1 in 3,562 nationally. That's 3,315 foreclosure starts in May alone, 10,099 across Q1. Tampa filed at 1 in 1,878; Orlando sits at 1 in 2,034.

Your options, from least to most damaging

1. Loan modification. Call your servicer's loss mitigation department before you miss a payment. Every major servicer has a dedicated number (listed in the Resources section below). FHA borrowers go through a specific loss mitigation waterfall: repayment plan, forbearance, standalone partial claim (arrears moved to a non-interest-bearing subordinate lien, repaid only at sale or refinance), then full modification (rate reduction, term extension up to 40 years). VA loans now have the new Partial Claim Program (launched June 15, 2026), which works the same way. Conventional borrowers can request a Fannie Mae Flex Modification targeting a 20% reduction in monthly principal and interest.

Servicers are more willing to work with borrowers who call early. Most options require a 3-month trial payment plan before becoming permanent. The earlier you call, the more tools they have.

2. Forbearance. If the hardship is temporary (3-12 months), forbearance pauses or reduces payments without triggering foreclosure. You'll repay the deferred amount later through a repayment plan, modification, or partial claim. Forbearance buys time for a temporary gap in income. If the carrying costs don't work even at full salary, forbearance delays the problem without solving it.

3. Short sale. You sell for less than you owe, with the lender's approval. You do NOT need to be delinquent to qualify. If you can document that your mortgage is unsustainable (imminent default), you can pursue a short sale while still current on payments, and being current gives you better negotiating position with the servicer.

Here's how it works in Florida:

Contact your servicer and request a short sale package. You'll submit a hardship letter (1-2 pages: the cause, the financial reality, your intent to cooperate), last 2 years of tax returns, last 2 months of bank statements for all accounts, last 30 days of pay stubs, a completed financial worksheet, your current mortgage statement, and a signed listing agreement with a purchase contract once you have an offer. Miss a document and the whole package goes to the back of the line.

The hardship letter matters. Qualifying hardships include job loss, divorce, medical emergency, death of a co-borrower, military deployment, disaster damage, and unexpected major expenses. Keep it professional, factual, and backed by documentation (termination letter, medical bills, divorce decree).

List the property with an agent who has real short-sale experience, or bring the lender a documented cash offer if the property condition or timeline makes listing unrealistic. Price from market value and repair condition, not from your loan balance. When you get an offer, the servicer's loss mitigation team reviews the hardship package, valuation, title items, junior liens, and approval terms. You can usually remain in the home while the file is under review, but you may still be responsible for insurance, utilities, maintenance, HOA dues, and other carrying costs.

The deficiency language matters. A short sale does not automatically erase the unpaid mortgage balance. The approval letter should say whether the lender is waiving the remaining balance, reserving rights, requiring a seller contribution, or reporting cancelled debt. Have a Florida real estate or foreclosure attorney review the approval letter before you sign. If the language is unclear, do not guess at what it means.

4. Deed-in-lieu of foreclosure. You transfer the property to the lender, skipping the court process. Credit impact is similar to a short sale. Not all lenders accept it, and some require you to attempt a short sale first.

5. Foreclosure. Last resort. Florida is a judicial foreclosure state, so the lender files a lawsuit. You usually have a short response deadline after service, and the timeline depends on the county, judge, lender, defenses, bankruptcy filings, and sale scheduling. A completed foreclosure can affect credit and may leave deficiency questions if the debt is not fully paid. Ask a foreclosure attorney how the risk applies to your file.

How long until you can buy again?

| Event | FHA | Conventional (Fannie/Freddie) | VA |

|---|---|---|---|

| Short sale | 3 years (1 year w/ extenuating circumstances) | 4 years (2 years w/ extenuating) | 2 years |

| Foreclosure | 3 years | 7 years (3 years w/ extenuating) | 2 years |

| Deed-in-lieu | 3 years | 4 years | 2 years |

Clock starts on the date the property title transferred, not when you stopped paying. "Extenuating circumstances" means a one-time, non-recurring event beyond your control (death of income earner, serious medical emergency). Requires documentation.

Tax implications of forgiven debt (this changed in 2026)

Debt forgiven through a short sale, modification, or foreclosure can create a federal tax issue, and lenders may issue a 1099-C when $600+ of debt is cancelled. Do not assume the forgiven amount is automatically tax-free or automatically taxable; insolvency, bankruptcy, principal-residence rules, and current federal law can change the answer. Florida has no state income tax, but you should ask a CPA or tax attorney before signing a short sale or deed-in-lieu agreement.

The insolvency exception may apply. If your total liabilities (all debts, including the forgiven mortgage) exceed your total assets (everything you own at fair market value) at the time the debt was forgiven, you may be able to exclude the forgiven amount up to your degree of insolvency. IRS Form 982 and Publication 4681 explain the calculation. Do not assume you qualify; ask a CPA or tax attorney before filing.

What NOT to do

Don't ignore it. Florida's foreclosure process is slow, which creates a dangerous illusion that you have time. By the time the lis pendens hits, your options narrow and the credit damage is already compounding. Contact your servicer at the first sign of trouble.

Don't drain savings to stay current on an underwater mortgage if the Holding Tax math doesn't work. If you're spending $4,000/month to hold a property that's losing $700/month in value and you don't have the runway to wait 3+ years for a recovery, you're destroying your cash reserves to delay the inevitable.

Don't hire a "foreclosure rescue" company. HUD-approved housing counselors provide free guidance (call 1-800-569-4287 or the HOPE Hotline at 1-888-995-4673 around the clock). Anything that costs money up front for foreclosure prevention is almost certainly a scam.

The Decision

| Your situation | Best move |

|---|---|

| Positive equity, home sitting unsold 60+ days | Reprice to 60-day comps, offer concessions, consider a cash offer |

| Condo with pending special assessment you can't afford | Sell before it records, negotiate a payment plan, or apply for Miami-Dade's loan program (786-469-4100) |

| Roof over 15 years, deals falling through on insurance | Apply for My Safe Florida Home, get roof certified, or sell as-is |

| Underwater by less than 10% | Bring cash to close if possible, or request a loan modification |

| Underwater by 10%+ with documented hardship | Short sale review with written remaining-balance language checked by counsel |

| Carrying costs exceeding $3,500/mo on a depreciating property | Sell now; the discount is cheaper than the bleed |

These four forces (repair mandates, insurance on one side, builder pricing and negative equity on the other) feed on each other. Special assessments spike HOA dues, which make units harder to insure, which shrinks the buyer pool, which drops values, which puts more owners underwater.

If you decide to wait, run your Holding Tax first. Don't guess at the number.

Resources

Servicer Loss Mitigation Contacts

| Servicer | Loss Mitigation Phone |

|---|---|

| Chase | 1-800-848-9380 |

| Wells Fargo | 1-800-678-7986 |

| Bank of America | 1-800-669-6650 |

| Mr. Cooper / Nationstar | 1-888-806-9263 |

| Rocket Mortgage | 1-866-316-2432 |

| NewRez | 1-866-214-5733 |

| loanDepot | 1-866-970-7105 |

HUD Housing Counseling (free): 1-800-569-4287 | Find a counselor near you

HOPE Hotline (24/7): 1-888-995-4673

Florida HUD-Approved Counseling Agencies

| Agency | Area | Phone |

|---|---|---|

| Neighborhood Housing Services of South Florida | Miami-Dade / Broward | (305) 751-5511 |

| Catholic Charities of Central FL | Orlando | (407) 658-1818 |

| Broward County Housing Authority | Broward | (954) 739-1114 |

| Housing Foundation of America | Pembroke Pines | (954) 923-5001 |

| Neighborhood Housing & Development Corp. | Gainesville | (352) 380-9119 |

| Wealth Watchers, Inc. | Jacksonville | (904) 265-4736 |

County Property Appraiser Links

Look up your assessed value, tax bill, exemptions, and building details (year built, roof type, square footage).

| County (City) | Website |

|---|---|

| Miami-Dade | miamidadepa.gov |

| Broward (Fort Lauderdale) | bcpa.net |

| Palm Beach | pbcpao.gov |

| Lee (Cape Coral / Fort Myers) | leepa.org |

| Hillsborough (Tampa) | hcpafl.org |

| Orange (Orlando) | ocpafl.org |

| Duval (Jacksonville) | duvalpa.com |

| Pinellas (St. Pete) | pcpao.gov |

| Collier (Naples) | collierappraiser.com |

| Volusia (Daytona) | vcpa.vcgov.org |

Key Programs and Contacts

| Resource | Contact |

|---|---|

| My Safe Florida Home (grants for wind hardening) | mysafeflhome.com |

| SHIP (county-level repair assistance, all 67 counties) | Contact your county housing department; find via floridahousing.org |

| Miami-Dade Condo Assessment Loans | 786-469-4100 / condospecialassessment@miamidade.gov |

| Condo Ombudsman | 954-202-3234 / ombudsman@myfloridalicense.com |

| DBPR Condo Division | 954-202-6831 / myfloridalicense.com |

| Florida Bar Lawyer Referral | 1-800-342-8011 ($25 for 30-min consultation) |

| Florida Free Legal Answers (low-income) | florida.freelegalanswers.org |

| FEMA Disaster Assistance | 1-800-621-3362 / DisasterAssistance.gov |

| SBA Disaster Loans | 1-800-659-2955 / lending.sba.gov |

| Citizens Property Insurance | citizensfla.com |

Property Tax Exemptions Worth Checking

If you're holding, reduce your carrying costs. Florida offers several property tax exemptions that many homeowners miss.

| Exemption | Statute | Benefit |

|---|---|---|

| Homestead | F.S. 196.031 | Up to $50,000 off assessed value |

| Save Our Homes cap | F.S. 193.155 | Assessed value can't increase more than 3% or CPI per year (whichever is lower); up to $500,000 of accumulated benefit is portable to a new FL homestead within 3 years |

| Senior (65+, limited income) | F.S. 196.075 | Additional $50,000 off (local option, not all counties) |

| Disabled veteran (100% service-connected) | F.S. 196.081 | Total exemption from property taxes |

| Widow / widower | F.S. 196.202 | $5,000 off assessed value |

All exemptions require filing by March 1 with your county property appraiser. The homestead exemption alone saves most homeowners $750-$1,000+ per year.

Frequently Asked Questions

Can I sell my Florida condo if there's a pending special assessment?

Yes. Known or pending condo assessments should be disclosed and checked against the contract, condo rider, association notices, and estoppel. Who pays can depend on negotiated contract terms, what has been formally adopted, and what the association reports before closing.

How do I find out if my condo building is SIRS-compliant?

Check the DBPR online portal. All associations were required to create accounts by October 1, 2025, and must submit a SIRS Reporting Form within 45 days of completing the study. If your building isn't in the database, it may be non-compliant. You have the right to request a copy of the SIRS report; the association must provide it within 10 business days of a written request.

Is My Safe Florida Home only for low-income homeowners?

No. Any Florida homeowner with an active homestead exemption, a home built before 2008, and insured value of $700,000 or less can apply. Low-income homeowners (at or below 80% of Area Median Income) get priority and don't need to match funds. Everyone else contributes $1 for every $2 from the state. Apply at mysafeflhome.com.

Can I get insurance on a roof that's 20 years old?

It depends on roof material, condition, remaining useful life, documentation, carrier underwriting, and the buyer's loan type. Private carriers or Citizens may ask for inspections, certifications, replacement plans, credits, or repairs. Check current insurance options before assuming the sale cannot close.

Is forgiven mortgage debt taxable in 2026?

It can be. Lenders may issue a 1099-C when $600+ of debt is cancelled, but the tax result depends on insolvency, bankruptcy, principal-residence rules, and current federal law. Florida has no state income tax. Ask a CPA or tax attorney before agreeing to a short sale, modification, deed-in-lieu, or debt settlement.

What's the difference between a four-point inspection and a wind mitigation inspection?

A four-point evaluates roof condition, electrical, plumbing, and HVAC. Most carriers require it for homes 20+ years old to get or keep coverage. A wind mitigation inspection evaluates storm resistance features (roof-to-wall connections, opening protection, roof geometry, secondary water barrier) and qualifies you for premium discounts. You want both. Bundle them with the same inspector for $150-$350 total.

How long after a short sale can I buy a home again?

FHA: 3 years (1 year with documented extenuating circumstances). Conventional: 4 years (2 years with extenuating circumstances). VA: 2 years. The clock starts on the date the property title transferred.

What is a deficiency judgment and can my lender come after me?

If your home sells for less than you owe, the unpaid balance can create deficiency risk. The exact risk depends on your loan documents, approval letter, property type, and legal path. Ask a Florida foreclosure attorney to review any short sale, deed-in-lieu, or settlement letter before you rely on it.

Need a clean number for your Florida house?

We buy Florida homes that need repairs, have insurance issues, or need a cleaner closing path. If a cash sale is one of your options, we can review the property and put the price, repair assumptions, seller costs, and closing timeline in writing.

(561) 258-9405Information current as of June 26, 2026. This guide is informational only; talk with a Florida real estate attorney, CPA, lender, or HUD-approved housing counselor before making legal, tax, mortgage, or foreclosure decisions.